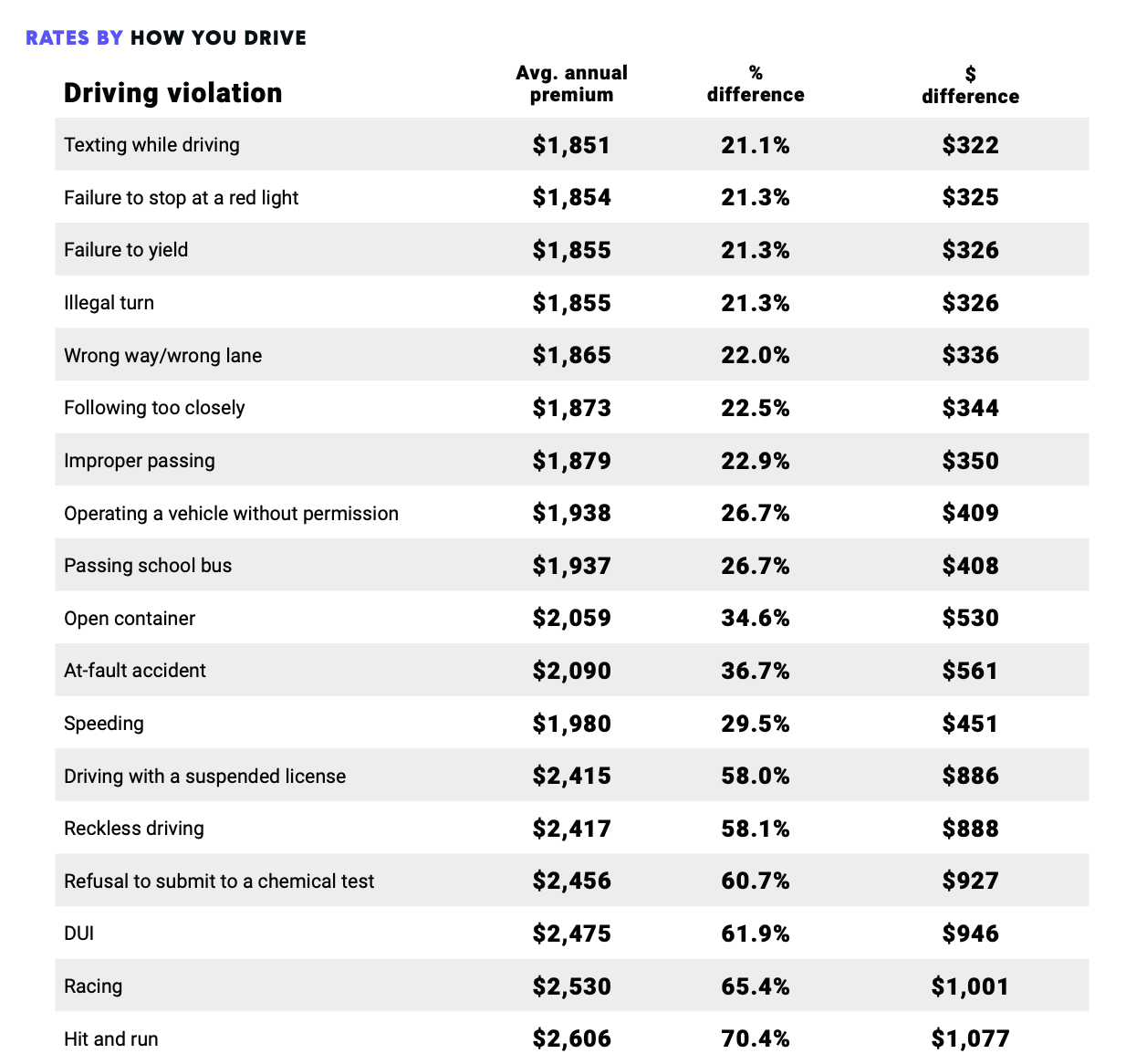

If you receive speeding tickets, run red lights or fail to heed other signals or signs on the roadway you are statistically more likely to cause damage to people and/or property. Thus, you are more likely to experience automobile insurance increases.

But how much is the increase, and will it ever go away? Keep reading for more from our NYC traffic violations lawyer.

Our clients frequently want to know how much of an insurance increase to expect if they are convicted of a traffic violation. Unfortunately, we can never give a specific answer. The amount of the increase and for how long you will be paying the increased rates depends on several factors, including the following.

While a first offense may very well lead to an increase in insurance rates, multiple moving violations are that much more likely to have an adverse affect on the amount you pay for automobile insurance.

If you have a long history of excellent driving while with a particular insurance company, it may take a little more to see a rate increase than it would for a driver with a similar driving history who is new to the insurance company.

Insurance is regulated by state law, and different states have different laws regarding automobile insurance requirements, penalties, and more.

Some states specifically prohibit insurance companies from raising rates under certain conditions while other states will require insurance companies to impose surcharges under other conditions.

In New York, for example, the law protects drivers with only one minor violation on their record over a certain time period but does not extend such protection to drivers with either two minor or one more serious violation over the same period of time.

Again, insurance companies are trying to determine which drivers are a safety concern and most likely to cause damage to people or property.

There is an inherent difference, for example, between an excessive speeding ticket and a traffic ticket issued for excessive use of a horn. That said, even minor traffic tickets can lead to an increase in insurance rates.

While there are many factors to consider and it is difficult for anyone to say exactly how much a traffic ticket will increase your car insurance, it is safe to conclude that traffic tickets generally lead to higher automobile insurance rates and the convictions for traffic violations should be avoided to the extent they can.

When someone receives a traffic ticket in New York, one of the primary concerns is a potential increase in automobile insurance rates. Clients ask all the time…”how can I keep my automobile insurance as low as possible?”

It’s hard to pinpoint exactly how much of an insurance increase a traffic ticket can cause. We will explore some ways to estimate how much your insurance will go up below.

Regardless of how much of an increase in insurance a traffic tickets may cause, there are a number of things you can do to help lower your existing insurance rates and keep them low moving forward. Look below to read some tips on keeping your insurance low.

Of all the actions that can be taken to keep insurance low, nothing compares to shopping around. Consumers who shop get better value for their insurance dollar than those who do not. It’s the single most proven and successful strategy when it comes to keeping car insurance low.

The automobile insurance industry is a competitive industry in general.

According to the New York State Insurance Department’s 2007 Consumer Guide to Automobile Insurance:

“There is active competition among auto insurers in New York

State…Rates can vary considerably among insurers…Therefore,

it is always a good idea to obtain quotes from several insurers.

Today, it’s more competitive than ever. Current economic conditions and credit issues have taken thousands of cars off the road and caused the cancellation of thousands of policies covering these cars.

Whether you have an excellent driving record or a poor record, a quick check just might show that you may be able to lower your existing rates.

if you have traffic tickets pending (issued but haven’t gone to court yet), now is definitely the time to check. On top of the competitive rates being offered, right now may be your best (and last) opportunity to take advantage of your record as it currently stands.

No matter your situation, you may be surprised to learn that auto insurance premiums for the exact same coverage on the same car can vary widely (by hundreds of dollars) between different insurers.

There are many websites that enable people to compare insurance quotes from some of the most popular insurance companies all at once. It takes only a few minutes and it can’t hurt to see if cheaper rates may be available from a number of top companies. While sites may differ, you should probably have your current registration handy to help answer some of the questions about your vehicle and have your current auto insurance policy handy to help answer questions about the type and amount of coverage you currently have.

There are steps you can take in New York to help reduce your auto insurance costs. Most, but not all, will apply to you.

Rates can vary considerably among insurers. Take advantage of a comparison website which enables you to get quotes from multiple insurers at once.

The best way to avoid auto insurance increases due to traffic tickets is to avoid receiving a traffic ticket. Drive safe and follow the rules of the road. If you are pulled over, read attorney Scott Feifer’s article offering some basic advice on what may help you avoid receiving a ticket in the event you are stopped by a police officer.

If you receive a NY traffic ticket, fight it. You are “not guilty” until proven otherwise. There is nothing on your driving record yet and your insurance company has no idea you received the traffic ticket. Do your research and consult with a traffic ticket lawyer early in the process to increase your chances of avoiding a conviction.

New York refers to it as the Accident Prevention Course. It removes four points from your driving record and is a “good” on your record to help offset the “bad” (convictions) in the eyes of auto insurers.

Make sure you are paying as little as possible for your automobile insurance. Paying less may be as simple as doing a little research and switching to a new provider. If you’d like to get quick quotes from other providers, get your vehicle registration and existing policy ready and click here (to our affiliate site)

For many people, raising the deductible on their auto insurance is a good way to cut the overall cost of the policy. Perhaps a mere increase from $250 to $500 can reduce your annual premium by 10 percent or more. Just make sure you can handle the larger deductible should the time come.

New York requires you to have liability coverage, but other non-mandatory coverages may be expendable. Be careful, though, of leaving yourself underinsured. Just because a type of coverage is optional doesn’t mean it’s not advisable to get it. There’s no requirement for anyone to carry life insurance yet it’s still a good idea…

Good credit is potentially important. Keep your credit in order an you are likely to enjoy lower auto insurance rates.

It’s about risk. In general, sports cars and other high-performance, flashy vehicles are classified as higher risks because they are common targets for thieves and because statistically, the people who own them tend to drive more aggressively. Owners of a Ferrari will likely pay a higher premium than owners of a Volvo station wagon or other low-risk vehicle.

Cars parked in garages are less likely to be stolen, vandalized, or struck by other vehicles. Using a garage to store your car may entitle you to a slight premium reduction.

You may receive discounts on your insurance if your car is equipped with one or more of the following options: anti-lock brakes, automatic seat belts, and airbags. Similarly, anti-theft devices such as car alarms and tracking systems (e.g., Lojack) may also get you a discount because they reduce the chances of your car being stolen or vandalized.

You may receive a discount from your insurance company if you buy more than one type of insurance through that same company (e.g., auto and homeowner’s). A discount may also apply to your auto insurance if you insure multiple cars under the same policy or with the same company.

This is when you authorize the insurance company to take your payment out of your checking account at the same time each month. This can save a little money each month.

As your car ages, it is worth much less than when it was new. Look up the Kelley’s Blue Book value of your car. That is the maximum amount your insurance company will pay if the car is “totaled.” You should review the collision and comprehensive coverages of your policy each year as your car gets older and decide whether it makes sense to continue paying for that coverage.

Don’t include other drivers under your car insurance unless you have to, especially younger drivers or those with poor driving records as they’ll only bring up your rates. Conversely, if you are a young driver, having an adult under the insurance can help lower your rates.

Wondering how much your insurance will increase after a ticket? Call Feifer & Greenberg, LLP today at (888) 445-9886 for a free consultation and to learn your options.

GOT A TRAFFIC TICKET? CALL OUR ATTORNEYS AT 888-842-5384

ANYTIME, WE’RE HERE TO HELP

FREE CASE EVALUATION

Please note that our website is an Attorney Advertisement. We do not recommend that anyone substitute anything they read or learn on the internet for personal legal advice from competent legal counsel.

Feifer & Greenberg, LLP, 15 Maiden Lane, Suite 508, New York, NY 10038, (888) 842-5384